“Empowering Smarter Business Decisions Through Data-Driven Insights”

Netherlands Remote Patient Monitoring and Telemonitoring Reimbursement Market Research Report Segmented by Reimbursement Scheme (Statutory Health Insurance Reimbursement, Bundled Care Reimbursement, Integrated Care Program Reimbursement, Innovation & Pilot Funding Reimbursement, Municipal & Community Care Reimbursement, Others); by Clinical Monitoring Area (Cardiovascular Monitoring, Diabetes Monitoring, Respiratory Disease Monitoring, Oncology Monitoring, Post-Acute & Surgical Recovery Monitoring, Elderly & Frailty Monitoring, Mental Health Monitoring, Others); by Care Delivery Setting (Hospital-Based Monitoring Programs, Primary Care Monitoring Programs, Home Healthcare Monitoring Programs, Community Care Monitoring Programs, Long-Term Care Facility Monitoring Programs, Others); by Monitoring Modality (Physiological Remote Patient Monitoring, Therapeutic Adherence Monitoring, Telemonitoring with Clinical Decision Support, Nurse-Led Telemonitoring, Physician-Led Telemonitoring, Hybrid Monitoring Programs, Others); by Provider Type (Receiving Reimbursement, Hospitals & Medical Centers, General Practitioner Networks, Home Care Organizations, Specialized Care Clinics, Long-Term Care Providers, Independent Telemonitoring Service Providers, Others) and Region – Forecast (2026–2030) Meta

- Report Code: VMR-19440

- Historic Range: 2023–2025

- Publish date: Jun-2026

GLOBAL NETHERLANDS REMOTE PATIENT MONITORING AND TELEMONITORING REIMBURSEMENT MARKET (2026 – 2030)

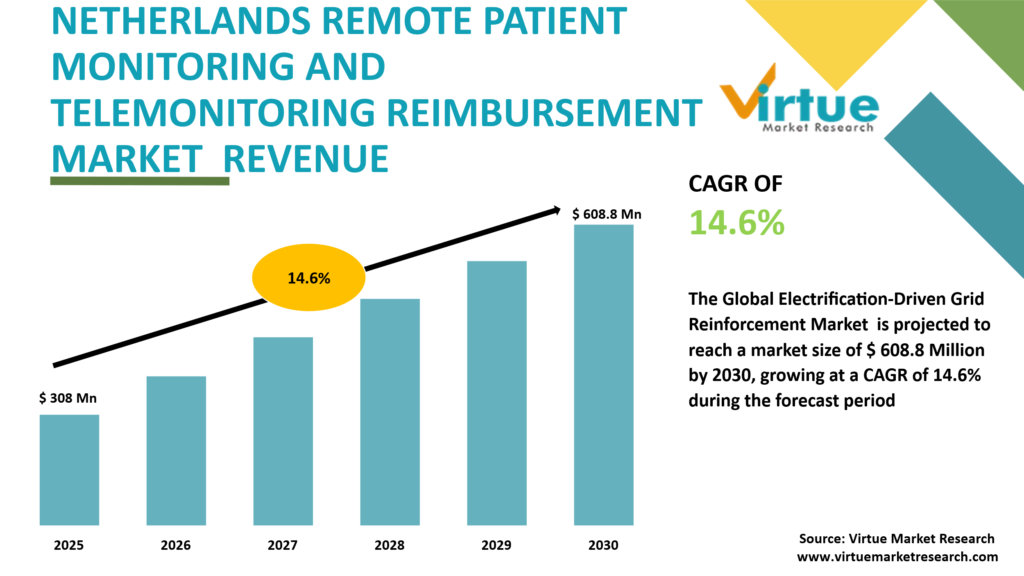

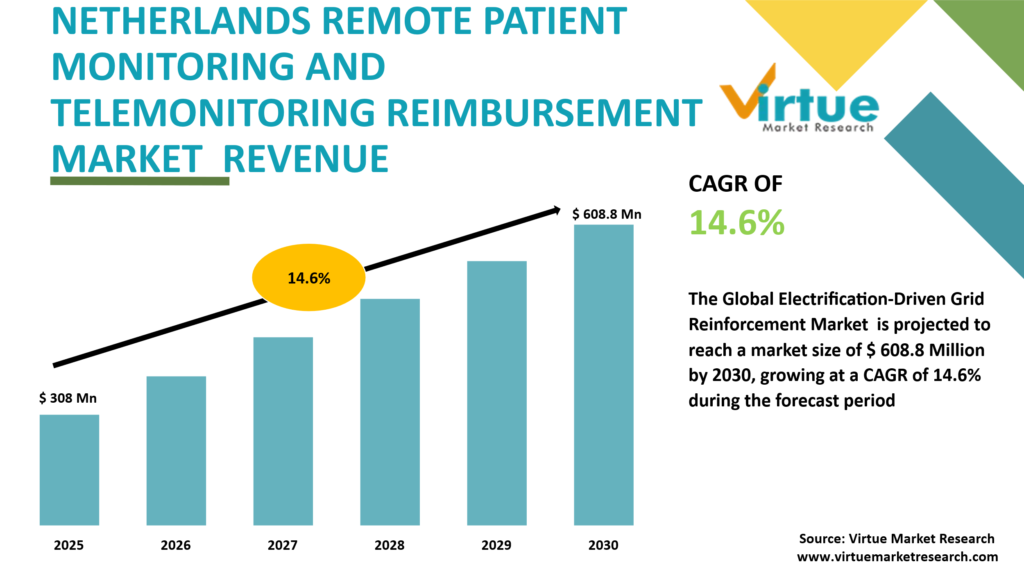

The Netherlands Remote Patient Monitoring and Telemonitoring Reimbursement Market was valued at approximately USD 308 million. It is projected to grow at a CAGR of around 14.6% during the forecast period of 2026–2030, reaching an estimated USD 608.8 million by 2030.

The Netherlands Remote Patient Monitoring and Telemonitoring Reimbursement Market is the healthcare reimbursement system that covers the digital healthcare delivery services provided by healthcare professionals to monitor patients remotely and intervene if needed. Topics covered in the market include funding approaches for remote clinical supervision, chronic disease management, recovery monitoring, and home health delivery. It covers reimbursement for professional monitoring activities and care coordination that incorporates telehealth, but not consumer wellness applications, non-clinical fitness tracking solutions or healthcare services not associated with structured remote monitoring reimbursement.

The market has grown beyond a few low-level pilots to include more frequent integration into the healthcare delivery system. Healthcare stakeholders have shifted to more scalable care models due to pressure on capacity, more chronic conditions, and the need for an ageing population to be managed. Therefore, reimbursement models are slowly moving from experimental funding models to models that encourage ongoing monitoring of patients and ongoing care management along multiple treatment tracks.

This shift is changing the strategic landscape for both providers and payers as well as digital health players. The key question has become how to find a reimbursement strategy that provides some measure of clinical benefit yet enhances efficiency. It seems that technology is not as key to market success as it was once thought to be and that sustainable funding structures, care integration, and provider participation are much more significant. By grasping these reimbursement dynamics, organisations can make informed decisions regarding growth, efficient resource usage, and adaptation to evolving healthcare delivery needs.

Key Market Insights

- 68% of contracted providers are putting more resources into remote monitoring.

- Almost 90% of executives consider monitoring devices very effective.

- 73% believe that wearables have a positive impact on detection and member engagement.

- The percentage of virtual health visits increased from 42% in 2022 to 44%.

- 94% of virtual-visit users are now interested in having another virtual visit soon.

- Over 70% of health care organizations made strides or achieved some degree of adoption of gen AI.

- A survey conducted at the end of 2024 showed that 47% of respondents had already introduced gen AI.

- Virtual wards will grow from tens of thousands up to hundreds of thousands.

- There is a potential worldwide market for remote patient monitoring of $78.4 billion by 2032.

- By 2029, the global market for smart hospitals will be worth $148.36 billion soon.

- More than $1 trillion in health care expenses could move through the decade.

- Over 40% of 2025 consumers already had a virtual visit.

- Eighty-five percent of CEOs believe there is a significant amount of transformation in healthcare coming in the near future.

- The pressure to automate monitoring grows with a 13 million nurse shortage by 2030.

Research Methodology Scope & Definitions

- The study measures the Netherlands Remote Patient Monitoring and Telemonitoring Reimbursement Market as the reimbursed value pool generated through approved remote monitoring and telemonitoring services.

- Coverage includes the Netherlands, historical analysis, base year estimation, and forecast period assessment.

- A standardized data dictionary, market boundaries, inclusion/exclusion criteria, and mutually exclusive segmentation framework are applied to prevent overlap and double counting.

Evidence Collection (Primary + Secondary)

- Secondary research utilizes verifiable sources including the Dutch Ministry of Health, Welfare and Sport (VWS), Dutch Healthcare Authority (NZa), National Health Care Institute (Zorginstituut Nederland), Statistics Netherlands (CBS), payer publications, provider disclosures, and company reports.

- Primary interviews cover healthcare providers, insurers, telemonitoring vendors, digital health specialists, reimbursement experts, and industry stakeholders across the value chain.

- Key claims are supported by source-linked evidence within the report.

Triangulation & Validation

- Market sizing combines bottom-up analysis of reimbursed monitoring activities and top-down assessment from healthcare expenditure and reimbursement allocations.

- Findings are reconciled against financial disclosures, utilization data, and expert interviews where applicable.

- Conflicting inputs are resolved through multi-source validation, consistency checks, and bias-control protocols.

Presentation & Auditability

- All assumptions, calculations, segmentation mappings, and forecasting models are documented and traceable.

- Tables, charts, and forecasts are linked to underlying evidence sources, ensuring transparency, reproducibility, and decision-grade auditability.

Netherlands Remote Patient Monitoring and Telemonitoring Reimbursement Market Drivers

Automated care delivery models are the focus of healthcare providers.

The growing workload of clinical activities is picked up by automated monitoring workflows in the healthcare sector in Dutch healthcare organisations. With remote patient monitoring, patients can be monitored at all times, and dependency on regular face-to-face communication can be minimised. The rollout of the reimbursement support for digitally enabled care pathways is shaping up to drive the modernisation of service delivery models and operational efficiency from setting to setting.

The adoption of telemonitoring is increasing with the use of clinical decision support tools.

As the use of intelligent clinical decision support grows, it is changing the way healthcare professionals are managing remotely monitored patients. With automated alerts, risk stratification functions and workflow optimisation tools, clinicians can quickly and effectively identify care needs and provide attention more efficiently. Various mechanisms are now being used to incentivise structured telemonitoring programmes, enabling scalable technology-based approaches to healthcare management.

Monitoring systems are transforming to a home-based approach.

Home-based health care is a growing priority in healthcare systems, with a focus on enhancing access and maximising the efficient use of facilities. The remote monitoring technologies will enhance patient engagement with the healthcare organisation in the context of a patient’s daily life and can be integrated into the general process of healthcare system modernisation. Reimbursement systems are increasingly recognising delivery of care with support from technology, and providers add capabilities to telemonitoring to enhance service continuity and efficiency.

Netherlands Remote Patient Monitoring and Telemonitoring Reimbursement Market Restraints

Impressive progress in digital health is undermined, however, by a lack of uniformity in reimbursement processes, poor integration of digital health systems, disjointed care coordination and a lack of integration within clinicians’ workflows. Expectations for data governance are constantly growing, and proving long-term economic value is still challenging. The lack of operational standardisation and provider capacity constraints also hinder the wider adoption of telemonitoring across care pathways.

Netherlands Remote Patient Monitoring and Telemonitoring Reimbursement Market Opportunities

Opportunities in the market include increased adoption of remote monitoring in chronic care pathways, growth in home-based clinical management, increased coordination between providers, and the use of intelligent monitoring workflows. With increasing emphasis on minimising avoidable use of the hospital and the collective desire for better long-term outcomes, there is further growth opportunity to be tapped into in a reimbursement environment.

How this market works end-to-end

- Patient Identification

Eligible patients are identified within cardiovascular, diabetes, respiratory, oncology, renal, elderly, or post-acute monitoring programs.

- Clinical Enrollment

Healthcare providers enroll patients into approved telemonitoring pathways based on reimbursement eligibility requirements.

- Technology Deployment

Monitoring devices, software platforms, and communication tools are deployed within home or community settings.

- Data Collection

Patient health information is continuously or periodically collected through remote monitoring systems.

- Clinical Review

Care teams review incoming data and assess patient status through established workflows.

- Intervention Management

Providers initiate interventions when clinical indicators exceed predefined thresholds.

- Reimbursement Coding

Monitoring activities are documented and aligned with applicable reimbursement frameworks and payment schemes.

- Payer Assessment

Health insurers and reimbursement bodies evaluate submitted monitoring activities according to program requirements.

- Provider Compensation

Hospitals, primary care providers, home care organizations, specialist clinics, and telemonitoring providers receive approved reimbursement payments.

- Outcome Evaluation

Stakeholders assess utilization, patient outcomes, operational efficiency, and future program expansion opportunities.

Why this market matters now

The Dutch healthcare sector faces a difficult balancing act. Demand for care continues to increase while workforce availability remains constrained. Telemonitoring offers a potential solution, but only when reimbursement mechanisms support routine implementation.

Many organizations assume technology adoption is the primary challenge. In reality, reimbursement certainty often determines whether telemonitoring remains a pilot project or becomes standard clinical practice.

Decision-makers must also navigate growing complexity. Different provider types operate under different funding structures. Clinical specialties face varying adoption rates. Budget pressures require stronger evidence of operational and financial value.

The result is a market where reimbursement intelligence has become as important as clinical effectiveness.

What matters most when evaluating claims in this market

Claim type | What good proof looks like | What often goes wrong |

Reimbursement growth | Verified payment pathway analysis and utilization trends | Reliance on pilot programs only |

Provider adoption | Multi-setting implementation evidence | Extrapolating from single institutions |

Clinical scalability | Long-term operational integration | Confusing pilots with sustainable programs |

Cost savings | Documented workflow and utilization impact | Assuming savings automatically occur |

Market opportunity | Defined reimbursement boundaries | Mixing reimbursed and non-reimbursed activities |

Patient impact | Measured clinical and operational outcomes | Using anecdotal success stories |

The decision lens

1. Define Market Boundaries

Verify exactly which reimbursed activities are included and excluded.

2. Assess Payment Stability

Evaluate whether reimbursement mechanisms support long-term deployment.

3. Compare Care Settings

Analyze adoption differences across hospitals, primary care, home care, and community care.

4. Evaluate Clinical Priorities

Identify disease areas where reimbursement support appears strongest.

5. Stress-Test Scalability

Determine whether programs can expand beyond regional or pilot implementation.

6. Examine Operational Readiness

Assess provider capacity, workflow integration, and monitoring resources.

7. Monitor Policy Signals

Track reimbursement evolution that could affect future adoption and investment timing.

The contrarian view

One common mistake is treating telemonitoring technology growth as equivalent to reimbursement growth. The two frequently move at different speeds.

Another error is assuming all clinical specialties face identical reimbursement conditions. Cardiology, diabetes, COPD, oncology, and renal care often operate under different adoption dynamics.

Buyers also frequently overestimate pilot activity. Pilot programs may demonstrate clinical value but not necessarily indicate sustainable reimbursement support.

Double counting can occur when monitoring activities are counted across multiple provider settings or reimbursement pathways. Robust market analysis requires a single reimbursement-value boundary.

Practical implications by stakeholder

Health Insurers

• Evaluate reimbursement sustainability across disease areas.

• Prioritize programs demonstrating operational efficiency.

• Assess long-term utilization implications.

Hospitals

• Align telemonitoring investments with reimbursable workflows.

• Identify specialty areas with scalable funding pathways.

• Improve capacity management strategies.

Primary Care Networks

• Expand remote monitoring capabilities where reimbursement supports continuity.

• Strengthen chronic disease management programs.

Home Healthcare Providers

• Position services around reimbursed monitoring models.

• Develop integration capabilities with clinical care teams.

Digital Health Vendors

• Focus on reimbursement-compatible solutions.

• Demonstrate operational and clinical value beyond technology features.

Investors and Strategic Buyers

• Assess reimbursement durability before evaluating growth potential.

• Examine specialty-specific adoption patterns.

Chapter 1 GLOBAL SOUTH KOREA DIGITAL THERAPEUTICS MARKET – Scope & Methodology

Chapter 2 GLOBAL SOUTH KOREA DIGITAL THERAPEUTICS MARKET – Executive Summary

Chapter 3 GLOBAL SOUTH KOREA DIGITAL THERAPEUTICS MARKET – Competition Scenario

Chapter 4 GLOBAL SOUTH KOREA DIGITAL THERAPEUTICS MARKET – Entry Scenario

Chapter 5 GLOBAL SOUTH KOREA DIGITAL THERAPEUTICS MARKET – Landscape

Chapter 6 GLOBAL SOUTH KOREA DIGITAL THERAPEUTICS MARKET – By Technology

Chapter 7 GLOBAL SOUTH KOREA DIGITAL THERAPEUTICS MARKET – By Component

Chapter 8 GLOBAL SOUTH KOREA DIGITAL THERAPEUTICS MARKET – By Prescription Model

Chapter 9 GLOBAL SOUTH KOREA DIGITAL THERAPEUTICS MARKET – By Distribution Channel

Chapter 10 GLOBAL SOUTH KOREA DIGITAL THERAPEUTICS MARKET – By Revenue Model

Chapter 11 GLOBAL SOUTH KOREA DIGITAL THERAPEUTICS MARKET, By Geography – Market Size, Forecast, Trends & Insights

Chapter 12 GLOBAL SOUTH KOREA DIGITAL THERAPEUTICS MARKET – Company Profiles – (Overview, Product TypePortfolio, Financials, Strategies & Developments)

Download Sample Report

Contact Us

- Chat On WhatsApp

- Phone :+91-9131799396

- Hi Link Residency, Airport Road, Indore, 452005

- sensegridmarketresearch@gmail.com

Select User License Type

Analyst Support, Customization & Verified Analysis

REPORT BY INDUSTRIES

- Food & Beverages

- Healthcare & Lifesciences

- Semiconductors & Electronics

- Information Technology

- Automotive

- Automation

- Energy & Power

- Consumer Goods & Services

- Agriculture